Rising Medical Inflation in India and Its Impact on Health Insurance Premiums

Medical inflation in India is rising fast. Learn how it impacts health insurance premiums and discover smart ways to manage rising costs in 2026.

Team Pazcare

This is some text inside of a div block.

Updated on:

March 31, 2026

Share

Table of Contents

Key Takeaways

Understand the reasons behind Rising Healthcare Costs! Dive into the impact of medical inflation on insurance premiums, fueled by technology tourism, and the Covid-19 pandemic. Discover strategies like copay and disease-wise capping to manage premiums while securing comprehensive coverage. Empower yourself to safeguard health without breaking the bank!

Understand the reasons behind Rising Healthcare Costs! Dive into the impact of medical inflation on insurance premiums, fueled by technology tourism, and the Covid-19 pandemic. Discover strategies like copay and disease-wise capping to manage premiums while securing comprehensive coverage. Empower yourself to safeguard health without breaking the bank!

Have you noticed an increase in healthcare expenses over recent years?

The rise in healthcare costs is caused by several factors, with Medical Inflation being one of them. The growing healthcare expenses linked to medical inflation can be concerning, whether it's the price of medicines, treatments, tests, or consultation charges. While having a health insurance plan can offer relief in managing expenses, it may still have various impacts on you.

In this piece, we'll explore the reasons behind medical inflation, how it influences health insurance and tips to tackle the issue.

Inflation in medical terms refers to the rising cost of healthcare goods and services over time. It reflects the increasing expenses associated with medical treatments, medications, hospital stays, and other healthcare-related expenses. This phenomenon contributes to the overall increase in healthcare expenditures, impacting individuals, healthcare providers, and insurance companies.

What are the causes of medical inflation in India?

Advancements in Technology

Medical technology advancements, particularly in cancer and heart disease treatments, aim to improve precision and effectiveness. However, the cost of developing such technology, including research, procurement, and training for imported machinery, costs a lot of time and money. The prolonged development duration and reliance on foreign technology contribute to the rise in overall healthcare prices.

Rise in Medical Tourism

India is known for providing high-quality healthcare services at reasonable prices. This has attracted global travellers to seek various medical treatments from India. International patients often seek services such as organ transplants, knee or hip replacements, or cancer treatments. This increased demand contributes to the overall cost of healthcare facilities.

High Demand for Healthcare Services

The advancements in medical sciences have increased their demand, leading healthcare providers to charge higher fees for treatments and procedures. The willingness of people to pay more for quality treatments further contributes to the upward trend in healthcare prices.

Effects of the COVID-19 Pandemic

The COVID-19 pandemic marked a pivotal moment in India's healthcare sector. The sudden surge in demand for medical equipment, such as ventilators and oxygen cylinders, led to an increase in healthcare prices. Additionally, there was a 10-20% rise in health insurance rates due to a rise in claims during the pandemic.

Increased Raw Material Cost

The increased cost of healthcare in India is also due to a high surge in prices for raw materials used in medicines and medical equipment. Additionally, higher import taxes, freight costs, warehouse fees, and emergency aid expenses also contribute to the overall increase in healthcare costs.

Change in Treatment Cost Per Person

Change in the treatment cost per person refers to the change in the cost of basic components of the treatment or medical procedure. This change is influenced by factors such as expenses for hospital consumables, personnel, consultations, and other costs associated with utilities, rent, or property.

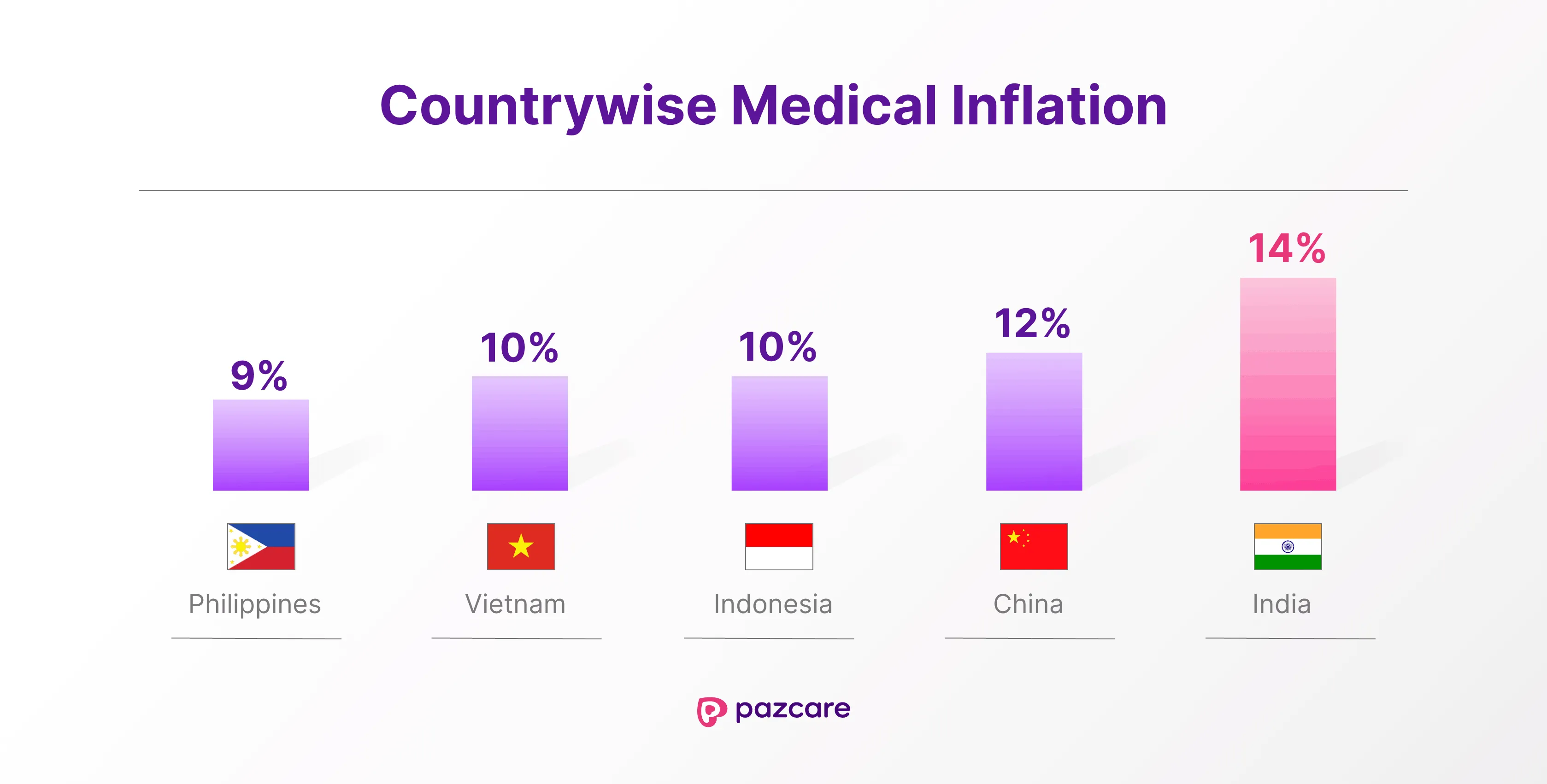

What are the current medical inflation rates in India?

According to recent estimates, the medical inflation rate in India is around 12.9%–14% in 2025–2026, making it one of the highest in Asia. In fact, some industry analyses suggest healthcare costs are rising close to 14–15% annually, significantly outpacing general inflation.

This sustained rise in medical inflation continues to directly impact insurance pricing. Earlier trends already showed a 16.5% increase in retail premiums and a 31% surge in group health insurance premiums, and insurers today still revise premiums periodically typically 10–15% every few years to keep up with rising claim costs.

How is this impacting health insurance premiums?

High medical costs burden insurers

With the escalating costs of medical treatment and healthcare services, insurance companies face an increased financial burden. Consequently, these companies are compelled to pay higher compensation, and ultimately, they pass on these elevated costs to customers in the form of higher premiums.

Transition to older age groups results in a premium hike

Health insurance premiums usually remain consistent within a specific age group. However, a premium change occurs when transitioning from one age group to another. Moving to an older age group may result in a significant rise in the premium, sometimes as much as 50%.

Severe impact on senior citizens and people with pre-existing diseases

Senior citizens and people with pre-existing diseases are more prone to requiring expensive medical treatments compared to younger individuals. Due to the higher compensation needed for senior citizens, insurance companies consequently raise the premiums for their policies.

How to manage rising group health insurance premiums caused due to medical inflation?

Introducing copay to parents and or or parents-in laws

A health insurance co-pay is a set percentage of the claim amount paid by the policyholder (employee), with the insurer covering the remaining portion according to policy terms. Opting for co-pay for either parents or all individuals in the GMC policy can effectively lower the premium.

Introducing disease wise capping

Certain diseases in an insurance policy have capped coverage, meaning the insurance company approves only a set percentage or specific amount for claims related to these diseases during the policy period. The policyholder (employee) is responsible for paying the remaining amount during hospitalization, thus reducing the premium.

To reduce insurance premiums, consider decreasing the sum insured. Ensure a balance between adequacy and affordability while aiming to lower the insurance premium.

How to manage rising retail insurance premiums caused due to medical inflation?

1.Purchase Health Insurance at the youngest age possible

Purchasing health insurance early ensures lower and more affordable premiums. These plans provide coverage for hospital bills and associated expenses, protecting you from escalating healthcare costs. The sooner you invest in health insurance, the better it is for both your well-being and finances.

2.Opt for No-Claim Bonus Health Insurance

Certain insurance companies often reward policyholders with no-claim bonus benefits for each year without claims. These benefits may include an increase in policy coverage or a premium discount. With every claim-free year, these benefits increase giving you a good way to improve your policy coverage and deal with rising medical inflation.

3. Choose a super top-up plan

Instead of only increasing your base sum insured (which raises premiums), consider a super top-up plan.

It provides additional coverage at a much lower cost

Activates after a deductible is crossed

Ideal for handling large medical bills caused by inflation

This is one of the most cost-effective strategies in 2026.

5. Go for a family floater plan (If Applicable)

Instead of buying separate policies, afamily floater plan can be more economical.

Covers multiple members under one sum insured

Helps reduce overall premium cost

However, evaluate carefully if you have elderly members.

6. Compare policies before renewal

Don’t blindly renew your existing policy.

Compare plans across insurers

Look for better pricing, benefits, and claim settlement ratios

Use digital platforms to find competitive premiums

Final thoughts

The progress in medical technology has enhanced the efficiency of the healthcare sector, meeting the rising demand for top-notch healthcare services. There are improved chances of treating conditions like cancer and heart disease. But these advancements come with a price.

Learning how to manage the increased premium rates caused by medical inflation can enable you to access top-notch healthcare without straining your finances.

Struggling with rising health insurance premiums? Pazcare helps you design cost-effective health plans that balance coverage and affordability so you don’t have to compromise on employee wellbeing

Key takeaways

Blog sources

About the Author

Follow on:

Thanks for subscribing! If it’s your first time, check your inbox. Otherwise, you’re already on our list

Oops! Something went wrong while submitting the form.

Ready to give yourself and your team the best employee benefit experience?

How much does group health insurance cost per employee in India?

Most companies pay ₹10,000-₹25,000 per employee annually, depending on coverage level, employee age, and company size.

What if treatment cost exceeds the sum insured?

Any expenses beyond the SI must be paid out of pocket. Employers can reduce this risk by adding a super top-up plan or enhancing the base SI.

How do you calculate group health insurance cost?

To calculate group health insurance cost, multiply the number of employees by the average premium per employee, then add any optional add-on costs and a renewal buffer.

Formula: Total GHI Cost = Number of Employees × Premium per Employee + Add-On Costs + Inflation Buffer

What is the cost of group health insurance in India?

The cost of group health insurance in India typically ranges between ₹3,000 and ₹15,000 per employee per year. The final premium depends on factors such as the sum insured, employee age profile, company size, industry risk, and selected add-ons like OPD or parent coverage.

How can companies reduce maternity-related insurance claims costs?

The most effective approaches include auditing and updating maternity sub-limits, tracking maternity claims separately from overall claims data, building pre-maternity wellness programs that reduce complication rates, improving employee awareness of cashless network hospitals, and exploring maternity-specific riders with insurers.

What is the average cost of maternity claims in Indian corporate health insurance?

Based on Pazcare's claims data, normal delivery claims in metro cities average ₹80,000–₹1,20,000, while C-section claims average ₹1,40,000–₹2,20,000 in the same settings. Costs vary significantly by hospital tier and city. Policies benchmarked against pan-India averages typically underestimate costs for metro-heavy workforces.

.svg)

.svg)